Opinion article based on @0xNonceSense post and my own research.

Polkadot and Cardano are very similar projects, one might even call them cousins. After all, both projects were founded by ex-Ethereum founders. Gavin Wood left Ethereum due internal conflicts and disagreements within the team, particularly regarding management and funding issues. Not very different to why Charles Hoskinson left as well.

In my previous article A History of Cardano’s Dramas and Controversies I covered the fact that Cardano was born from controversy within the Ethereum founding team, and Pokladot’s history is very similar as well. Afterwards, both projects took different paths and made different decisions regarding how to build their blockchain and which trade-offs to make. But it’s interesting to note that both projects started off from the same place of “rebellion”.

The Funding

Cardano’s Initial Coin Offering (ICO) ran before Polkadot, from September 2015 to January 2017. While Polkadot’s first round took place in October 2017. Cardano’s strategy was to focus on Japanese investors to avoid the compliance gray zone that plagued the United States. While Polkadot had a more global target market, it was still heavily focused on Europe and Asia for the same reasons.

Cardano raised 108,845 BTC, initially valued at $62 million, by selling 25.9 billion ADA of the 45 billion or 57% of the total supply. At current market value, the bitcoin raised during the ICO would now be worth $11.7 billion dollars. With the current market capitalization of Cardano sitting at $20.85 billion dollars, some quick math shows a 78% return on investment (ROI) so far.

Polkadot has had several funding rounds besides the first one that took place in October 2017. In total the project raised $247.76 million dollars in four rounds. If instead the Polkadot project used the money raised to buy bitcoin, they could have bought around 57,100 BTC. Today they would be worth $6.15 billion dollars. Meanwhile, the current market capitalization of Polkadot is $5.48 billion, which provides us with a negative ROI of -10%.

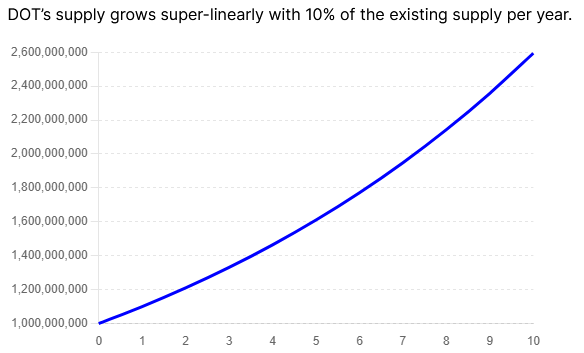

How could this happen? Very technically similar projects (Polkadot’s consensus algorithm is based on Cardano’s Ouroboros) after eight years yield such different results. One reason could be related to their so-called “redenomination” which took effect on August 21, 2020. Polkadot redefined its token units so that 1 old DOT would now be equal to 100 new DOT. The smallest unit of account (a Planck, similar to Lovelaces on Cardano) remained unchanged, but the DOT decimal point was shifted two places, from 12 to 10 decimal places. This change increased the total supply from 10 million to 1 billion DOT.

Although this redenomination did not constitute a dilution, since everyone’s proportional ownership remained unchanged, increasing the total supply hundredfold is not a small change in tokenomics. More so, since Polkadot unlike Cardano does not have a hard limit on supply. Just like Ethereum, there’s no limit to the amount of DOT that will ever exist. This creates a downward pressure on price, if liquidity is not able to sustain the valuation.

Lesson to be learned: There have been some discussions in the Cardano ecosystem regarding the maximum supply of 45 billion ADA. Some voices have raised the topic of increasing or removing this supply limit. However, this limit has now been ratified by the constitution but it does not mean it can’t be changed in the future. One sneaky way to do it would be a similar path that Polkadot took, by changing decimal places.

The Treasury

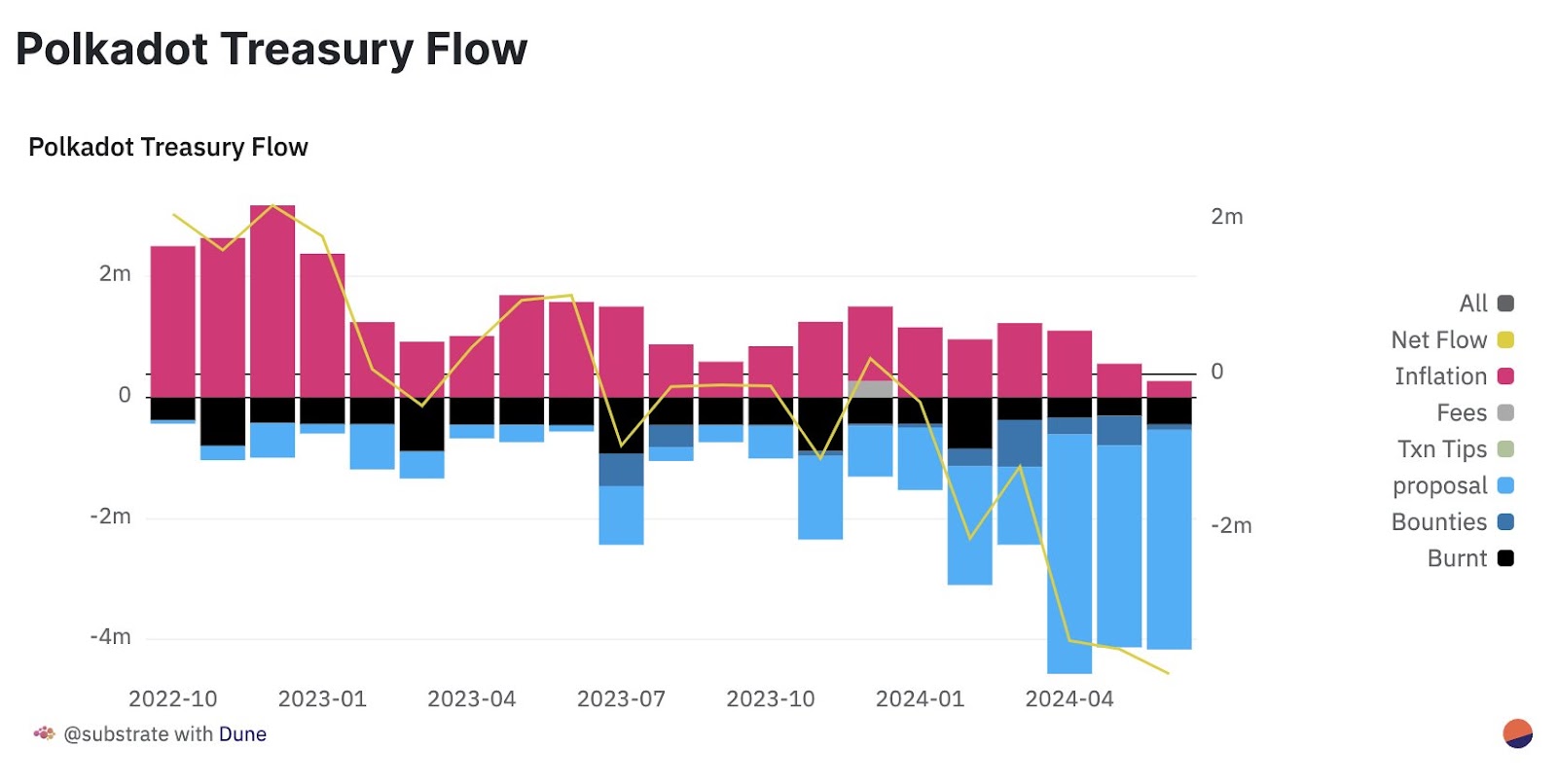

Perhaps the biggest mistake that Polkadot made was regarding the mismanagement of their treasury. By the first half of 2024 they had spent $87 million dollars of which $36.7 million was spent on outreach. These are mostly marketing proposals by the community for things like: $500 thousand to put an animated logo on the Coinmarketcap homepage. $10 million dollars for sponsoring a race car driver, a football club and an esports event. $4.9 million was spent on influencers and digital ads. $7.9 million was spent on conferences and events. $1.2 million for Gavin Wood and parachain teams to attend the World Economic Forum (WEF).

You might think these expenditures are justified to make Polkadot more popular and well known, however the Polkadot treasury has been burning funds faster than they go back in while also providing a lot of selling pressure on the open market.

Another problem that they are having is the inflation of the network, related to the previous point of not having a maximum circulating supply. With an annual inflation rate of 10%, which they argue is to incentivize staking rewards so honest actors secure the network, the value of DOT is being diluted on top of the mismanagement of funds.

There’s another similarity between Polkadot and Cardano treasury management and that’s diversification. The Cardano treasury is currently only composed of ADA (1.7 billion with a market capitalization of just over $1 billion dollars, at the time of writing this article). However, Charles Hoskinson is currently pushing to diversify it, by selling ADA and buying stablecoin USDM (in which he personally invested) and BTC.

I’m not personally against the idea of using the Cardano treasury, for example back in February 2025 I posted on X about my idea of the “Ouroboros Sovereign Fund” in which we employ the ADA saved from the Libertarian Budget Proposal to provide much needed liquidity to the main organic stablecoins from the ecosystem (DJED, iUSD, USDM and USDA). I will cover more about this topic in a future article.

However, the problem arises when you are selling your own ecosystem token for another ecosystem token (in this case BTC). The message sent to the market is that BTC is more valuable than ADA. The effect on price is even worse if it’s communicated publicly and with a lot of time in advance (it has to be due to the nature of governance on a public chain).

You can actually see in the ADABTC chart, after the initial mention during an AMA on June 8 regarding the idea of converting $100 million dollars from the treasury into BTC and stablecoins, ADA lost 23.46% against BTC in 20 days (so far).

In the case of the Polkadot treasury, it currently only holds DOT and stablecoins in the form of USDC and USDT to provide liquidity on DeFi protocols. But it doesn’t hold BTC at the moment, although the community has already proposed it. I would strongly advise against it, since it would be the last nail on the coffin for DOT.

Lesson to be learned: Selling your ecosystem token to buy another ecosystem token only tells the market that your token is less valuable. Why? Because the only reason for exchanging asset A for asset B is, if asset B is more valuable than asset A.

It would be different for example, if we use the ADA from the treasury (which is not floating in the open market) and instead of selling it, we lock it in the DJED protocol to mint DJED and SHEN. Which could be used to provide liquidity across different DeFi protocols.

The Governance

Governance on Polkadot has also had a very interesting journey and one which the Cardano community should pay very close attention to. Polkadot uses a decentralized governance system called OpenGov, introduced in 2023, to allow anyone with DOT tokens to propose, vote on, and enact changes to the network.

Polkadot’s governance is also one step ahead of Cardano, having moved from a centralized governance system to a decentralized one. This has been one of my main critiques of CIP-1694 and the centralized nature of the supposed “decentralized governance on-chain” that was marketed as. In my article Why Governance on Cardano Will Fail I pointed out this issue and quoted @nullHashPixel thread on X/Twitter in which they propose the implementation of Switzerland’s direct democracy system.

The old council model centralized power, slowed down innovation, and excluded the broader DOT community. OpenGov replaced it with a scalable, decentralized, and transparent system that aligns with Polkadot’s founding vision: a fully governed chain by its token holders.

Under the old system, governance was largely driven by a small, elected Council and an appointed Technical Committee, which had disproportionate control over proposal selection, emergency upgrades, and treasury spending. This structure limited transparency, made participation difficult for average users, and often resulted in bottlenecks and slow decision-making.

Public proposals were rarely prioritized unless endorsed by the Council, which discouraged grassroots involvement and innovation. Voter turnout in Council elections was low, and decision-making processes were often opaque.

OpenGov was introduced to address these issues by enabling any DOT holder to submit proposals, vote with conviction-weighted influence, and participate in a transparent, on-chain process with parallel decision tracks. The new system supports continuous governance, removes centralized gatekeeping, and better reflects Polkadot’s vision of decentralized and scalable protocol evolution.

OpenGov is Polkadot’s next-generation governance system that replaced the earlier “Council and Technical Committee” model. It emphasizes decentralization, continuous decision-making and track-based logic. Any DOT holder can submit a proposal, provided they bond DOT as collateral (refunded if the proposal is accepted or rejected gracefully). The amount of bonded DOT depends on the track the proposal enters.

A very interesting functionality they have is the conviction multiplier, a mechanism in Polkadot’s governance that lets DOT holders increase the weight of their votes by locking their tokens for longer periods. It rewards long-term commitment to the network while discouraging short-term manipulation and lets smaller holders have more influence, if they’re committed. It’s a good mechanic that seeks to counter the asymmetrical disadvantage of wealthy individuals and entities on a proof-of-stake governance system.

Lesson to be learned: Cardano is going through its first year of real governance, after many years of experimenting with Project Catalyst (with mixed results). Polkadot has already walked this path of centralized decisions making committees that Cardano is currently on. I’m sure OpenGov also has its issues and challenges, but at least as an outside observer, it seems a better path to reach real decentralized governance than the centralized corporate structure of Intersect.

Conclusion

Polkadot’s demise is not the result of one bad decision, but rather the accumulation of several strategic missteps: misaligned tokenomics, questionable treasury management, and a series of optics and execution issues that compounded over time. Despite its technical similarities to Cardano and shared ideological origins in the Ethereum fallout, Polkadot’s trajectory highlights how critical execution and governance are in shaping a blockchain’s long-term success.

The contrast between Polkadot and Cardano is a cautionary tale for every blockchain ecosystem: having a good idea is not enough. How you fund it, how you manage your resources, and how you engage your community through governance all play a central role in determining success or failure. Polkadot’s decision to redenominate, its lack of a fixed supply, and its treasury spending have all contributed to eroding confidence, even as it made meaningful strides in governance with OpenGov.

For Cardano, the lessons are clear. Respect tokenomics. Be thoughtful with treasury diversification and the messaging it sends. And learn from those who’ve already taken a misstep. Decentralized governance holds promise, but only if it’s built transparently, inclusively, and with strong safeguards against the mistakes of the past.

I learned a lot from this article, thank you.