The term co-opt has its origins in the Latin “cooptāre”, which means “to choose” or “to pick”. The concept of cooptation implies various forms of inclusion, assimilation or control within different contexts such as politics, organizations or social groups.

In this article I will explain why I believe that Bitcoin is being co-opted by the banking system, and if the Cardano blockchain could face the same path.

Bitcoin has been designed as a revolutionary technology to compete with traditional banking systems and fiat monetary systems, as a decentralized digital currency.

Thanks to Bitcoin, the brilliant invention of Satoshi Nakamoto, blockchain technology has gained a lot of attention due to its ability to provide secure, transparent and efficient transactions without the need for intermediaries.

That sparked the interest of several banks, which have already begun to incorporate DLT (Distributed Ledger Technology) technology in their operations, such as Bank of America, JP Morgan Chase, BNP Paribas, Commonwealth Bank of Australia, Deutsche Bank, Federal Bank of India , UBS, and many others. Article.

These institutions are adopting blockchain to improve various aspects of their operations, such as cross-border transactions, fraud prevention, security, identity verification, and smart contracts.

As Bitcoin continues to gain ground, traditional bankers face the challenge of adapting to this new financial landscape and more and more banks around the world are offering bitcoin services to their clients, understanding that their large market capitalization presents it as the number one in the crypto industry. And of course, where there are money flows, there are the bankers.

Forms Of Cooptation

But not everything is paradise, since the mass adoption of Bitcoin comes at a cost: there are more and more regulations and State interference in the development of Bitcoin.

Could you tell me that blockchain is decentralized and uncensored, and that politicians cannot interfere or control the Proof of Work algorithmic consensus, but you will see that there are oblique ways to violate these principles, which I will explain. You can also read an article I wrote two years ago about how regulations can attack Bitcoin, which I left at the end (1).

For the entry of “hard” money into the Bitcoin market, that is, institutional money, laws are required that allow this type of innovative investment, which has only been a little over 10 years since its birth and popularization.

Many in the crypto space applaud the influx of institutional money, as it drives up the price due to demand for this scarce commodity (at least so far, the algorithm is designed to issue 21 million, and no more).

And yes, Bitcoin is seen as an investment product by many, even the guys on Wall Street, although its utility was supposed to be “A Peer-to-Peer Electronic Cash System” according to the Whitepaper, and not digital gold.

Thus, bankers understand the potential, and instead of fighting Bitcoin as dangerous competition, lobbying the politicians of the day to seek regulations to ban or stifle Bitcoin, they have decided to co-opt it, i.e. adopt it to suit their needs, and thus be able to control it.

Since Bitcoin operates outside the realm of traditional financial systems, bankers must navigate complex regulatory frameworks to ensure compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations.

The regulatory challenge bankers face in adopting Bitcoin also turns out to be a tool to be able to control it, and have banker intervention digest the course of money, something bankers throughout history have been very clear about.

And precisely that challenge is the spearhead to seek regulations that allow its use and adoption, but also its control.

Besides, the low scalability of blockchain technology poses a challenge for its mass use.

The current Bitcoin infrastructure is limited in terms of transaction processing capacity, which may make it difficult for banks to adopt it for large-scale operations.

But precisely this limitation will seek to be exploited with intermediation and custody, offering centralized, faster and less expensive services.

This limitation in scalability is related to self-custody, where millions of wallets interact with the blockchain to carry out transactions, and it is only possible to record a limited number of operations in 1 MB blocks every 10 minutes, (with the implementation of SegWit Up to 4MB upload is possible).

In the case of third-party custody, a “few” wallets carry out a smaller number of transactions (although involving huge sums of money, the so-called “whales”), managed on centralized exchange platforms where clients’ holdings are only records in a database that intermediaries (bankers) manage.

You have to be clear that when you have your BTC deposited in an exchange you do not have the keys and you do not interact with the blockchain when you buy or sell BTC, but you are only a creditor of an amount of BTC and your debtor is the exchange.

Imagine if there were no self-custody, no one would have a wallet and everyone would have their bitcoins in a single exchange, the only one in the market, okay? The only one that would make all the transactions on the blockchain would be that exchange, and there would be no scalability problems. Of course this is an extreme example to get the idea across.

One more step in the same sense of co-option, are Bitcoin ETFs.

Bitcoin ETFs (Exchange-Traded Fund) are a regulated financial instrument and can be spot or futures.

Spot ETFs have actual Bitcoin as an underlying asset, allowing investors to participate in the Bitcoin market without directly owning the cryptocurrency. Futures ETFs use Bitcoin futures contracts to expose themselves to the price variations of the cryptocurrency at a specific date in the future.

ETFs are traded on traditional exchanges, making it easier for institutional and individual investors to participate in the cryptocurrency market.

Spot Bitcoin ETFs track the price of Bitcoin in real time, while futures ETFs may have costs associated with rolling over or liquidating futures contracts.

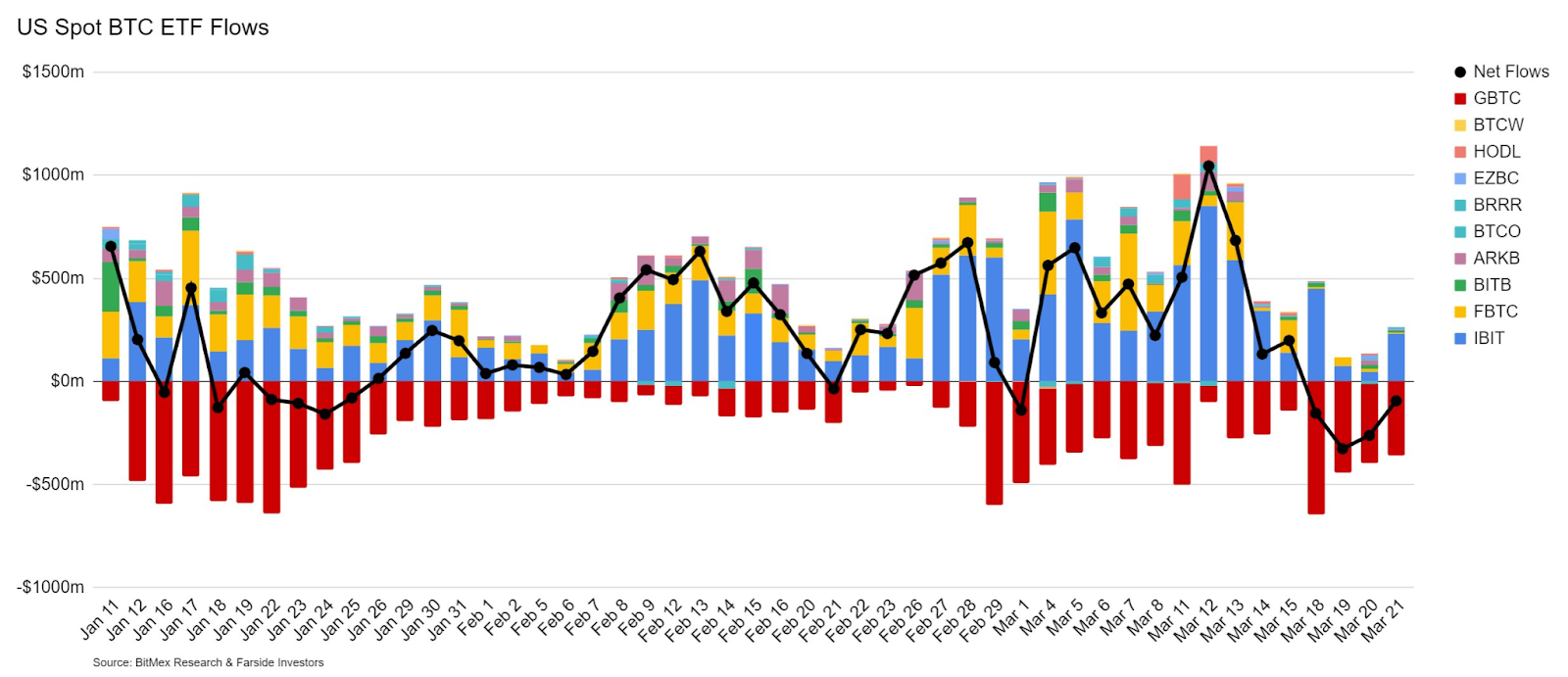

BTC futures ETFs have already existed for years, while on January 10, 2024, Bitcoin spot ETFs were approved by the SEC (Securities and Exchange Commission).

In the following graph you can see the flow of money handled by the Bitcoin ETFs of the different authorized managing funds:

Could Cardano Be Co-opted By The Banking System?

The quick answer is yes, it is possible. But there are mitigating factors.

Bitcoin’s market cap is ~60 times larger than Cardano’s, as of this writing, and growing: Bitcoin surpasses silver to become the eighth largest asset by market cap, and that data is one of those that attracts the banking system. But over time, I understand that the capitalization of Cardano will tend to grow, because the price will tend to rise, as long as demand grows, and that will seduce Wall Street investors.

Cardano is a blockchain just like Bitcoin, and both support sidechains, however Cardano has a richer programmable structure, and this makes the wide variety of developments possible, using smart contracts and native NFTs.

Cardano is perhaps more comparable to Ethereum, due to its third and second generation design structure, respectively. Incidentally, the network created by Vitalik Buterin is much closer than Cardano to being co-opted by bankers, with development and governance being notably centralized compared to Cardano, and institutional investors really like that.

As I said, Cardano’s programmability enables a large number of developments in its ecosystem, and it could happen that some of them arouse the interest of traditional market investors. In this context, in a first stage it could happen that there was no interest in the Cardano blockchain, its L1 layer.

This flow of investments from venture capitalists could encourage investment in Cardano as a complete ecosystem, and with clearer regulations, bankers would arrive.

There is a key point, Cardano was intended by its founder Charles Hoskinson to comply with regulations: “Find a healthy middle ground for regulators to interact with commerce without compromising some core principles inherited from Bitcoin” which can be read in its Whitepaper Why Cardano.

Final Words

In this article I have raised the co-option of Bitcoin by bankers, as something that I understand to be negative.

Following the Cypherpunk philosophy, the crypto space was designed to generate a means for individual freedom and autonomy, but I know that many are not interested in this vision, and only see this new technology as a new dynamic means of investment and speculation.

I really like the author Buckminster Fuller, and one of his quotes says: “To change something, build a new model that makes the existing model obsolete” and for that the new model must be differentiated and not co-opted, since it would end up being the same model only with some new features.

In short, having read this article, whatever your position on the crypto space, I hope it has been useful to understand the current landscape of this industry.

Bonus: At the time of writing this article, a book called “Hijacking Bitcoin: The Hidden History of BTC” by Roger Ver(*) is about to be published on April 5, 2024, which among other topics, deals with the influence of banks to control BTC.

(*)Roger Ver is a San Cristobal native known for being one of the first investors in emerging companies related to Bitcoin, who after the block size debate and the BTC fork, is one of the best-known evangelizers of Bitcoin Cash.

. . .

(1) Regulations Will Attack Bitcoin Decentralization