What is the downside of buying and holding NFTs? There is risk, of course, as the floor price could drop and profit could be lost. There is also the disadvantage of locked liquidity. To date, the holder of a high dollar NFT only has two options: hold on to it and have the funds locked up or sell it to access liquidity. Fluid Tokens intends to present a third option: the ability to receive short term loans on NFT assets. This means that you can hold an NFT for the long term and have access to ADA for other investments. They are describing it as the “first ever generalized bridge between NFTs and DeFi”. Basically it’s a peer to peer lending platform where NFTs can be used as collateral. How is all of this going to work? Let’s have a look.

Loans are nothing new. The borrower pledges to repay the original amount plus a premium. This premium is what incentivizes the lender to assume the risk of lending the money. There are, of course, entire industries built around this in traditional finance – banks, mortgage companies and so on. DeFi is revolutionizing traditional finance by removing the need for the middleman and therefore making things faster, more efficient and less expensive. Fluid Tokens is using smart contracts and the security of the Cardano network to take the next step, allowing one individual to loan funds to another with the NFT as collateral. All of the Smart Contracts for Fluid Tokens are written in Plutus and fully on chain. Only the front end interface which allows the wallets to connect is off chain.

How It Works

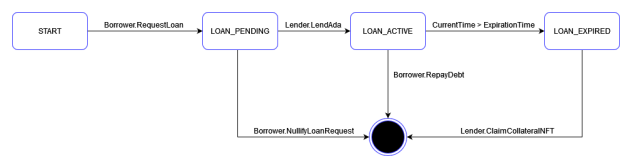

The team is rolling the project out in several layers. The first is pretty straightforward. There is one lender and one borrower and a series of Smart Contracts that will only execute when the correct conditions are met. The borrower requests a loan. Initially this is as simple as listing the NFT that will be used as collateral, requesting a loan amount, time frame and repayment amount. Lenders can review all of the open requests and choose which requests to participate in. This means that if the borrower sets unattractive terms, few lenders will choose to engage in a loan. Once a lender commits to the agreement, the NFT is locked in the smart contract and the ADA is released. The borrower can repay the loan and retrieve the NFT at any time up to the time that the contract expires. Here is a diagram from the Fluid Token Whitepaper:

A few things to note:

- Initially all transactions will be in ADA. Fluid Tokens just announced a partnership with COTI that will allow the integration of Djed into the platform. This will allow borrowing / lending without worry of price fluctuation.

- The loan premium, or interest, is determined at the beginning and does not change if the borrower repays the loan early.

- The only thing that is locked in the smart contract is the NFT.

- To avoid congestion related problems, there is an hour added to the contract time. This means that if the borrower repays at the last possible second – there will still be a grace period for the payment to be received before the asset can be claimed by the lender.

- The NFT remains locked in the smart contract until the payment is made or the lender claims it. This means that even if the time has expired, the borrower can still repay the loan and reclaim the asset – until the lender claims the NFT.

- All parties must communicate through the smart contract.

- Lenders do not pay any fees other than blockchain transaction fees. Borrowers do pay a fee to Fluid Tokens.

- No KYC is required from either party. This is a strictly permissionless system.

The Token

Fluid Tokens intends to release a token of its own. This will facilitate a DAO form of governance which will allow holders to propose changes and vote. Additionally, there will be a reduction of borrower fees for token holders. At a later date Fluid Token holders will receive a percentage of platform fees. The Whitepaper states that more use cases for the token, such as airdrops, are being investigated. No specific tokenomics were listed at this time beyond the fact that there will be a cap of 100 million tokens. Eventually a percentage of platform revenue will be returned to token holders, although specifics have not yet been released.

Longer Term Goals

As mentioned, the first version of Fluid Tokens is a pretty straightforward peer to peer lending mechanism. The borrower requests, the lender agrees, the NFT is locked until payment is received. They are planning for some significant upgrades as the ecosystem matures. They are investigating the creation of investment funds that will allow broader and more sophisticated usage. Additionally, time and usage will allow Fluid Tokens to provide data and insight for both users and borrowers as to how the loans are working for different collections.

The Positives

- The platform will allow NFT holders access to liquidity while continuing to hold their assets.

- The system is permissionless – no KYC is required.

- The team is available and engaging with the community.

- The recently announced Djed partnership will provide additional options and room to grow.

The Negatives

- This is a brand-new idea and there is little precedent to follow. Unexpected things could happen.

- There is risk for borrowers in that you could lose an asset that is much more valuable than the loan.

- There is risk to the lender that the floor price of the NFT could drop and, if the loan isn’t repaid, the full amount is not recoverable

Final Thoughts

As with any brand-new platform, trying to assess Fluid Tokens is rather like trying to read tea leaves. So far, the idea is interesting and the team open and engaging. If successful, it will allow NFT holders much needed access to liquidity. The risks are largely related to the lack of precedent- with anything this new, unforeseen complications can arise. As always, every individual should assess their individual risk tolerance and do their own research.

If you are interested in learning more:

Twitter: @FluidTokens

Website: Fluid Tokens