This post was adapted from a thread originally posted by @Flantoshi on Twitter

On paper, 2021-2022 sound like atrocious years – civil unrest, supply chain collapses, record-breaking inflation, growing authoritarianism, a possible world war, and (who could forget?) a pandemic raging behind the scenes.

This could well be the background lore for a shlocky sci-fi novel. But it’s likely to continue being our everyday life for the foreseeable future. It’s not unreasonable to think that the bill has come for the economic and social excesses of the last decade.

The Piper must be paid, and thus with a heavy heart, we must admit that a painful economic recession is on the horizon. History may not repeat itself, but it most certainly rhymes.

That said, this time around we have one element which had hitherto not existed as a substantial enough force on the world stage – CRYPTO.

Any way you look at it, from normal user penetration to government and corporate adoption, crypto is poised to be a powerful force in the years to come. This change in the equation might lead to entirely different situations than one might expect.

In this article, we will explore what will happen in an upcoming economic crash, and how crypto will play a pivotal role in shaping the world that comes after it.

The Usual Playbook

Rather than get bogged down in the specifics of the little financial nightmare we’re concocting, let’s sidestep that altogether. Let’s not worry whether it was inflation, or deflation, or a little Gremlin called Albertson who likes to golf on Wednesdays. For some reason, the economy collapsed and people now trust companies and governments so little that they intend to do something about it.

At this point, if history is any guide, there is the so-called “flight to safety” where people with financial interests rapidly derisk and flee to assets that are perceived to be safe, such as US Dollars, Swiss Francs or Gold.

But let’s make the situation more interesting as well. Let’s say either people can’t exchange their assets for those other ones, or they have their own problems and are not desirable. The US Dollar has been faltering as a reserve currency, the Swiss Francs are made of chocolate, and private gold ownership has a long history of getting banned.

After all, capital controls, where governments tell you what you can and can’t do with your money, are the favourite of faltering economies. That or just outright stealing what you own and giving you precious little in recompense.

However, there’s a sense of smugness that usually underpins these types of discussions “Sure,” they’ll say “I admit this can happen elsewhere, but not in X country because of our democracy / developed economy / constitution / take your pick.”

So, rather than talking in generalities, let’s talk about specifics – a core Euro member who behaved little better than a third-rate dictatorship when push came to shove. And I dare say is a fantastic model of what might happen if the situation gets dire enough in developed countries, as it did what it did at the behest of the European Commission and the International Monetary Fund.

The year was 2012, and the world was still reeling from the Great Recession of 2008. The crisis had revealed several flaws in the world financial system, among them the fact that Greece had been cooking the books for decades to get into the EU in the first place, as there are theoretically very high barriers to entry.

Naturally, countries that had invested in Greece under the pretence of the fake numbers suddenly realized that their investments were bunk. This was the position that the Mediterranean nation of Cyprus found itself in, and to further add complications, their banks were also overleveraged with local property companies, among many other contributing factors.

The situation was rather grim, and this insolvency eventually reached a climax – either something drastic needed to be done, or the whole economy of the island would collapse.

By June 25th 2012, the Cypriot government requested a bailout from the EU authorities, citing the aforementioned reasons. Naturally, people panicked as they suspected that their money is in danger, so the typical flight to safety to other assets begins.

However, not long after, restrictions were imposed. Transfers abroad were limited and cash withdrawals were capped at up to EUR300 per day! (It’s worth mentioning these restrictions didn’t disappear until 2014 for the cash withdrawals, and 2015 for the capital controls, respectively) This caused an uproar, and businesses began only accepting cash, as they rightfully suspected that any money that ended in the banks would, in turn, be subject to restrictions and/or confiscations.

Long story short, the Cypriot Government, the financiers, and the powerful intragovernmental agencies, eventually came up with “The Economic Adjustment Programme for Cyprus”, which had an interesting provision:

The Cyprus Popular Bank, then the second-largest bank in the country, would be restructured. As part of the changes, a portion of it was to be folded in with the Bank of Cyprus, the largest bank in the country. Accounts under EUR100k would be saved, while 47.5% of accounts above this threshold would be seized and forcefully exchanged into bank shares.

This was euphemistically called a “bail-in” when what it really was, was the theft of client money to be able to repay bad debt that they had no hand in creating.

It’s kind of the funny thing about the world we live in, often when we describe events exactly as happened, even just calling a space a spade sounds overly conspiratorial. But the truth is simple, as long as you play their game, you play by their rules.

Those in power don’t consider any money you have to be *your* money, but merely its temporary custodians until there’s a good enough excuse to take it away from you. If they could guarantee it was a more efficient system, they’d prefer to give you the least amount of access to private property as possible – just look at the broader historical record.

It’s no coincidence that widespread slavery was abolished just in the midst of the industrial revolution when machines were able to outcompete raw human brawn but required someone cooperative who didn’t throw a wrench in the fragile works if they got too angry.

The freedoms that those in power give to the plebs are given either because they fear their collective ire, or because it’s seen as an acceptable trade-off given what they can offer in return.

Crypto changes the equation somewhat as suddenly the average person gains the ability to sidestep any and all restrictions placed on them. Suddenly it’s the powers that be having to play catchup to the terms created by the plebs, which is an utterly intolerable way of operating for the elites.

Flight to Crypto

Even as far back as the Cypriot financial crisis a decade ago, we already started seeing signs of people fleeing to cryptocurrencies amidst all the restrictions. It was still early days for Bitcoin, so commentators at the time were very surprised by people’s flight to crypto, as they dismissed the asset class altogether.

Yet, even so, it was so intense that BTC went up by 176.2% in March 2013 alone!

It’s far from the exception as well. Perhaps the first battleground for crypto as an actively used currency counter to the government’s wishes is likely to be Venezuela. Where despite the government trying to limit crypto directly by blocking websites where you can buy it, it’s seen a massive boom in the country.

Venezuelans have gotten really creative since they have had their backs against a wall, as their economy is destroyed by communist-driven hyperinflation. They’ve even gone as far as repurposing old satellite TV dishes to send and receive Bitcoin peer-to-peer.

The Venezuelan authorities have failed so badly at the task of limiting crypto’s adoption that blockchain analysis firm Chainalysis actually rate Venezuela as being seventh in the top 10 of the 2021 Global Crypto Adoption Index.

Similar stories can be found all over the world, from Nigeria to Turkey, to China. As crypto was typically designed from the bottom up and doesn’t require centralized custodians, it’s a novel set of circumstances for governments.

The authorities are baffled by this change in the rules of the game. Look no further than the Canadian authorities threatening cryptocurrency exchanges so that they wouldn’t tell their customers to self-custody their crypto.

Recently, Canada has turned somewhat authoritarian in their efforts to crack down on the truckers who are refusing to get forcefully vaccinated for COVID-19. Whether you agree or not with mandatory vaccinations is beside the point, as the important thing is how the Canadian authorities are addressing this matter.

They started by limiting protestors’ access to crowdfunding platforms, then proceeded to freeze personal accounts and go against people who aided them in any way (even those who just gave them coffee). They want to make these individuals be unable to live their lives unless they agree with the political views of the government.

But they’ve hit a snag with crypto as it’s an alien world.

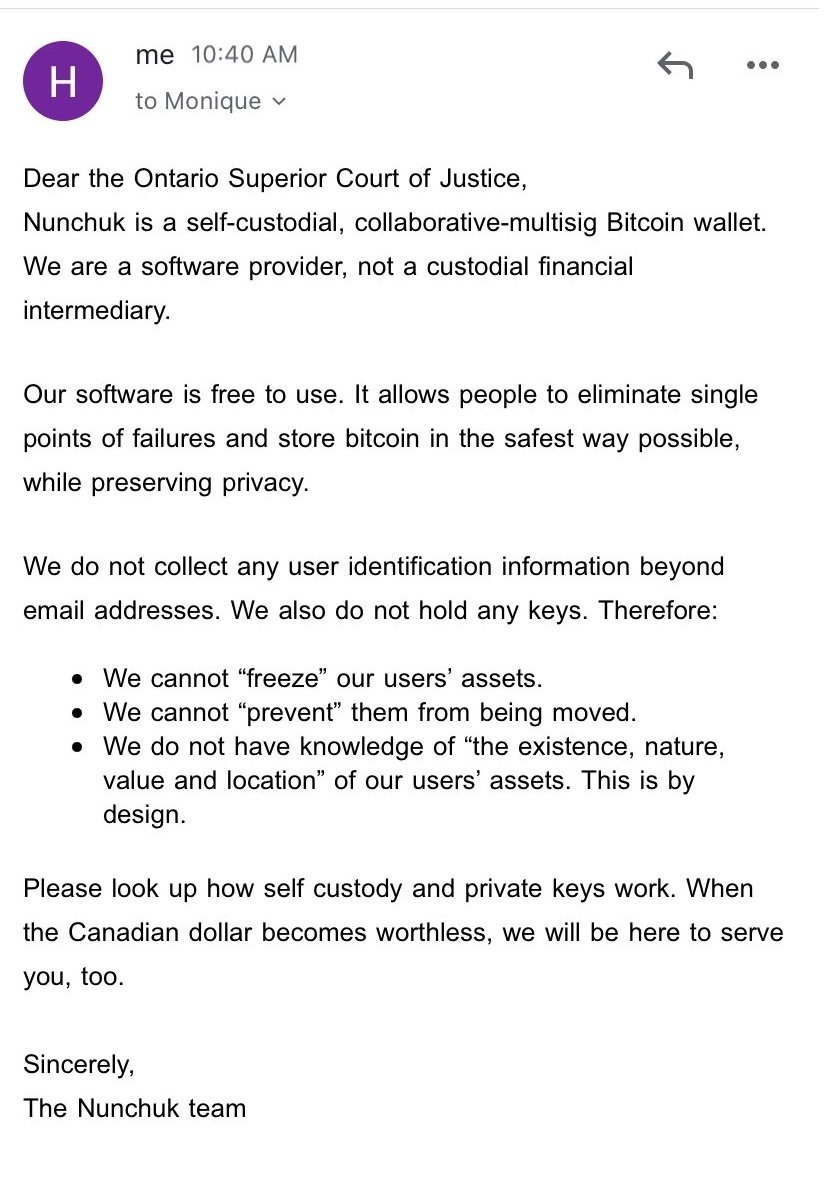

On February 18th 2022, the Ontario Superior Court of Justice sent the open-source Bitcoin wallet Nunchuck.io a Mareva Injunction, which ordered them to freeze and disclose information about the assets involved in the Freedom Convoy 2022 movement. Their response was amusing, to say the least:

The point of the matter is that the weapons that the elite used to use to cajole and force the plebs into submission are increasingly not as effective as they used to be. That’s the terrifying promise of crypto, where if people don’t agree with the aims of the authorities, they can potentially be sidestepped entirely.

Crypto, while not a panacea, gives the common citizen the ability to be as financially sophisticated as they wish, while not immediately beholden to any national authorities.

The Shadow Economy

Charles Hoskinson, the founder of Cardano, has speculated that as crypto becomes more widespread, and the available arsenal of tools develops, it’ll become increasingly difficult for tax authorities to be able to clamp down on it. Eventually, they’ll simply have to give up, and focus on taxing elements that they can control, such as increased property and consumption taxes (VAT and the like), as this type of financial activity is much more difficult to hide.

Most people don’t want trouble, they want a simple and easy life where they’re not subject to the arbitrary whims of those above their social station. For the most part, the average person is able to tolerate a lot before they start going out of their way to be non-compliant.

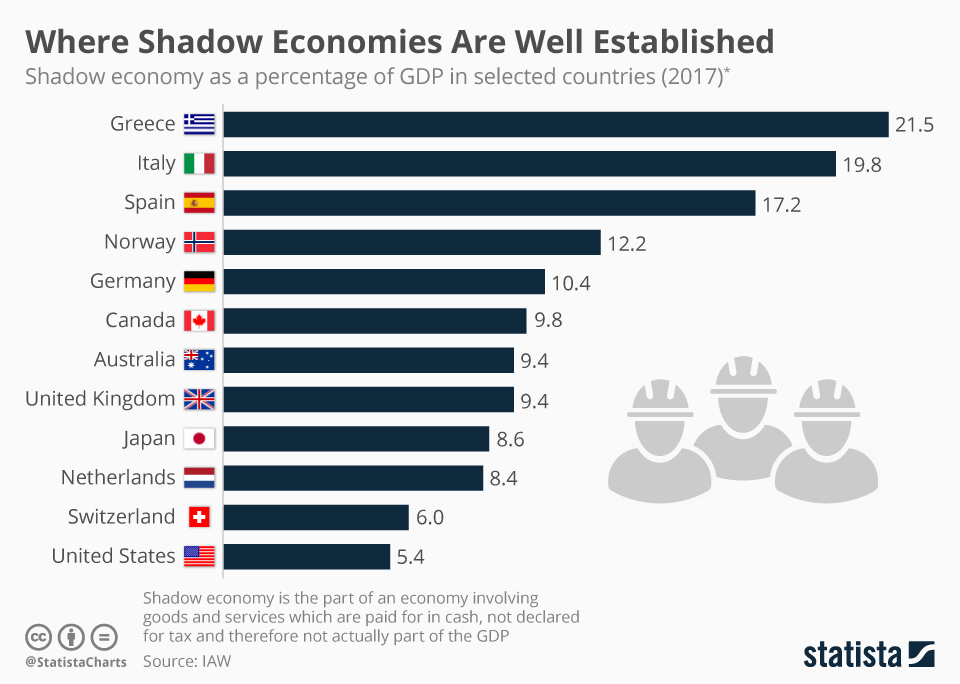

But once you’re on their bad side, it might take generations to recover, if it’s possible at all. For example, in Greece, owing to its hundreds of years of occupation by the Ottoman Empire, there’s a culture of deep distrust against the government.

So much so that it’s commonplace for businesses to have two sets of account books – one you show to the taxman and the other one that contains the real information. It’s been estimated that up to 23% of the Greek economy is unaccounted for and thus part of the “Shadow Economy.”

At this point, tax dodging is part of the Greek character, to the point where politicians have joked it’s the national sport.

Now, while the wounds inflicted by government overreach in the face of an economic collapse might not be quite as severe as that of an occupying force being present in the nation for hundreds of years, the same broad principle applies. People will start fleeing via crypto and trying to transact with it.

The problem though is that due to its relative novelty as an asset class, crypto is extremely volatile. It’s not unreasonable to assume that it is likely to be close to impossible to run a business with low-profit margins and high variable costs through it.

Imagine if you were to run a burger joint and have your prices at fixed ADA costs. Minute to minute your profit margin is changing, as your costs are in another currency. So, an order might earn you money in one moment, while five minutes later you might be losing money with the same transaction.

That’s why, for the most part, the few businesses that accept crypto have done so as a marketing ploy, or because they’re die-hard crypto fanatics. Viewed uncharitably, rational companies are gambling that the interest brought by signalling that they accept crypto is greater than the customers who will actually take them up on their offer.

In other words, it’s not done out of a serious desire to use it as a means to run a business. This is the main reason mainstream crypto will remain an oddity and unable to grow in to replace national economies, it’s simply too volatile.

It’s not particularly new criticism I’m bringing here though, as it’s been an open secret for quite some time in the crypto community. In fact, the whole sub-industry of so-called “stablecoins” has surfaced as a means of creating a relatively robust type of money that doesn’t wildly fluctuate from moment to moment.

But as crypto as a whole develops, the stablecoin sub-industry has changed. Originally, we just had stablecoins where a centralized custodian would back a token with deposits that they had under their control.

The problem is that this just recreated the single points of failure that crypto purports to solve in the first place. Centralized custodians like Tether aren’t just like banks, they’re worse than banks. Whereas banks now have hundreds of years of regulation and auditing somewhat curbing their worst excesses, these new financial entities do not have any such oversight.

They’re often purposefully domiciled in jurisdictions where authorities will turn a blind eye, or give them far more leeway than would otherwise be tolerable. Yet, if push comes to shove, they can still freeze accounts holding their currencies.

Obviously, this is intolerable for anyone who genuinely believes in the potential of cryptocurrencies to unbind the wider public from the tyranny of the elites. And so, other alternatives have come to the surface.

Algorithmic Stablecoins are stablecoins that can function independently from centralized entities. These tokens have a previously agreed on price target that they seek to maintain parity with through a complex interplay of algorithms. In order to maintain their peg, these coins run a set of instructions that limit or increase the available supply of the tokens, so that their market value remains in line with their target.

There are many specific methods by which you can create stablecoins and which one is ultimately more effective is beyond the scope of this article. For now, let’s simply say that these algorithmic stablecoins are a developing use case by which you can create a widely held source of value that is easy to transact and remains at a predictable price point.

It bears mentioning that due to the open-source nature of most crypto projects, this will soon be a technology that is widely available to the public. And there’s nothing in the protocol that fundamentally restricts its users in mimicking the value of preestablished assets like the USD, CHF, EUR, or gold.

The technology underpinning algorithmic stablecoins can be used to create coins pegged to literally any number, no matter how bizarre or specific. Do you want a coin pegged to the kilo price of Arabica coffee beans or the number of Wikipedia edits on the page for Michael Jackson?

It’s entirely possible to create this. So money’s going to be able to change and take forms it has never taken before.

Social Money

One easy mistake that people make when talking about crypto is to completely ignore the social aspect of money. Money does not exist in a vacuum, it has to be actively used between communities of people to exchange value for it to be worth anything.

In a previous article, we went into detail about how the notion of money will change by broadening to an extent that is hitherto unimaginable. Consider if every DAO, every major corporation, and every town is able to have their own currency that is usable within its borders.

It sounds needlessly confusing but it is a by-product of creating decentralization. If we aim to be decentralized and flexible enough to weather economic shocks, then our very notions of what value is must be diversified.

As bizarre as it might sound, it’s not the first time this has happened either, especially in times of crisis. At its core, money is a tokenized abstraction of the social favours owed to the bearer thereof.

So it can come in any and all shapes as long as a large enough group of people is willing to honour the value of the scrip. A good example thereof is Ireland in 1970 where all the banks closed down for over half a year and were operating at a very reduced rate for months thereafter.

In the years leading up to the crisis, there were several bank staff strikes, and in 1970 the largest one took place. As such, for over a year, and with little warning the Irish populace was left with very little banking infrastructure. Curiously though, banks were fairly seamlessly replaced by pubs overnight and the economy actually grew!

While the arrangements were rather slapdash and improvised, what happened was a combination of using the money already in circulation, and existing businesses that knew their customers well ran a ledger system where debts were tallied, IOUs were settled and credits were given to trustworthy patrons.

Initially, people thought this affair would only last a few days, but it dragged on for weeks and months instead. It’s unlikely that something of the sort could be repeated in the current world, as people in modern urban environments tend to operate anonymously, and don’t have enough information about their neighbours to know whether they can trust them or not.

But fortunately, crypto is able to fill the void lost. Cardano, for instance, is already trying to build some notion of verifiable reputation on the blockchain which can be used to transact with others, even if one does not know their real-life identities.

All in all, if I were to summarize the promise of crypto it is that we will be able to transact on our own terms with people, and in ways that have become impractical as societies have grown. As such, we will be able to benefit from the operational efficiencies of working at scale, while being able to work at an individual level where people are more than numbers on a spreadsheet.

If push comes to shove, the wider public is gaining the ability to shut the government from financial transactions in general, and it’s a terrifying and thrilling prospect. It’s my hope that through these means we can renegotiate the social contract to be more equitable for all!

Conclusion

I’m writing this conclusion just as Russian troops are marching into Ukraine, and crypto has not been a hedge in the slightest for real-life turmoil.

The flight to safety narrative for crypto is somewhat eroding, it’s becoming clear that it is an asset class like any other, a very speculative one at that – so it’s unlikely to be the first place that people flee to when shit hits the fan. With all that said though, it still remains a wonderfully flexible asset class that you can use to move billions of dollars in value within minutes and with very little oversight.

Not only that, but if you know what you’re doing, you can completely bypass government restrictions, and conduct business on your own terms (this is not legal or financial advice, just stating the fact that the protocols allow it).

You can’t fully ever ban crypto, a single willing person only needs to have an account abroad to buy it online, and suddenly they can bring millions of dollars in crypto instantaneously through the border, which they can trade at a markup for things like gold. Even in countries where there are mild capital market restrictions, we already see this, for instance, Bitcoin sold in South Korea carries a so-called “Kimchi premium” on it.

So crypto is certainly something that countries will have to embrace rather than fully fight. Some other time we’ll discuss how governments can wield crypto regulation to destroy any promise that the tech has.

But for now, what we can say with certainty is that it’ll remain a powerful force that the populace can use to escape government overreach, and in turn build parallel economies that rival the traditional power structures.

I do think we live in interesting times where the world will be utterly unrecognizable by the end of it. Whether it ends up being heaven or hell, remains yet to be seen. What I do know with certainty is that whichever future we choose, crypto will play a role in it.

If you’re in the crypto or in the traditional finance industry looking for someone to ghostwrite content for you, please do not hesitate to message me. I’m a full-time ghostwriter.

Join the community over at @flantoshi on Twitter.

And if you would like to support this project and help me pay rent, I’ll pass on the tip hat and you can send ADA to:

addr1qxfgs44d763uuw4hy6qatx383v9mmrrm6qazay6eren9sp5r2usruecwv33lp2t2nqp4ss6hrc9ac8yd2klxnsfnxz2qw3su4s

Thank you for your support!